|

The Constitution directs the UT Board to establish a distribution policy that provides stable, inflation-adjusted distributions to the AUF and preserves the real value of the PUF Investments over the long term. To achieve these goals, the UT Board has adopted a "percent of assets" spending policy for the PUF. Under this policy, the distribution rate is set, currently 4.75% of the prior twelve quarters' average net asset value of PUF assets, and therefore dollar distributions vary with the volatility inherent in financial markets. Although this policy exposes distribution recipients to relative high volatility and may result in the loss of nominal or real purchasing power in yearly distributions, it is effective in maintaining the purchasing power of the PUF corpus. This policy was chosen for the PUF because it best suits endowments in which current distributions are small relative to the total budget of the beneficiary and where long term growth of the endowment fund is the key objective as is the case with the PUF.

However, the UT Board does not have unlimited authority to set the PUF distribution rate. Distributions to the Available University Fund are subject to the following overriding Constitutional requirements:

- Distributions must be at least equal to the amount needed to pay debt service on PUF Bonds;

- Distributions may not increase from the preceding year (except as necessary to pay debt service on PUF Bonds) unless the purchasing power of PUF Investments for any rolling 10-year period has been preserved;

- Distributions may not exceed 7 percent of the average net fair market value of PUF Investments in any fiscal year, except as necessary to pay debt service on PUF Bonds.

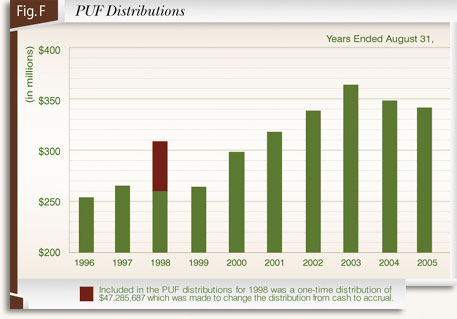

Distributions from the PUF to the AUF decreased by 2.0% from $348.0 million in fiscal year 2004 to $341.2 million in fiscal year 2005. This decrease reflects the fact that the average net endowment value, which is the amount used to calculate the distribution, is based on a three year quarterly average and was calculated using the twelve quarters ending with the February, 2004 quarter. Thus, the average net endowment value, which is multiplied by 4.75% to determine the fiscal year 2005 distribution, still reflects lower net asset value quarters in 2001 and 2002. As these earlier net asset value quarters are replaced in the calculation by the higher net asset values of the past two years, distributions will begin to increase. For example, the FY 2006 distribution is $357.3 million, an increase over the FY 2005 distribution. Figure F shows the ten year history of PUF distributions.

Click to print charts in this section using PDF format

Click to print charts in this section using PDF format

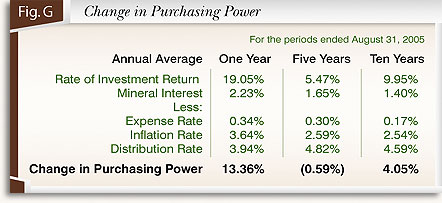

As depicted in Figure G, the PUF has achieved the objective of maintaining its inflation adjusted value because purchasing power has increased over the ten year period by 4.05%. Fiscal year 2005 provided real growth in the PUF of 13.36%. This growth is retained in the PUF to offset years, such as fiscal years 2001 and 2002, when investment returns trailed the inflation rate and purchasing power was not maintained. The rate of investment return in Figure G is the gross total return. The net investment return reported in Figure E is net of investment management fees. The expense rate in Figure G includes both investment management fees and other fees.

|